Fort Lauderdale News from Fort Lauderdale, Florida • Page 73

- Publication:

- Fort Lauderdale Newsi

- Location:

- Fort Lauderdale, Florida

- Issue Date:

- Page:

- 73

Extracted Article Text (OCR)

NcwsSun-Sentinel I a invesiors watcnmg cioseiy for breakthrough on AIDS Stock tables Sunday, Sept. 1, 1985 i Section Trouble in ComputerLand reflects industry market research firm, Data-quest tracks trends throughout the high-technology field, from personal computers to semiconductors. "When the industry was growing it was easy to hide business mistakes, but it has become a mature market," DeWitt said. "And although we're expecting a 13 percent increase in unit sales nationally by the fourth quarter due to Christmas sales, across the whole industry there's no growth at this time." sales this year. But the demand for home computers still considered an untapped market since only about 13 percent of U.S.

households have one has yet to fully materialize. And corporate customers, who are behind two-thirds of the personal computer industry's $26 billion in hardware sales, are now sitting on the sidelines, DeWitt said. "American business is pausing to Please see COMPUTERLAND, 2E Representatives of Dynamation Enterprises which holds the Miami franchise, have been unavailable for comment, but former employees have said the business also became caught between withering consumer demand and the cost of maintaining substantial inventories. The slackening of demand for personal computers nationwide has surprised even the experts. Just six months ago, Dataquest was forecasting a 49 percent increase in dependent relationships with major vendors, industry sources say.

Such a shake-out will likely continue for ComputerLand the nation's largest computer retailer with 630 stores and other companies as well. "It boils down to increased competition and low margins, and ComputerLand is by no means the only retail channel experiencing difficulties," said Norm DeWitt, a personal computer industry analyst for Dataquest Inc. A San Jose. Also last week, 12 ComputerLand stores in Atlanta closed, bringing to 26 the number of franchised stores that have gone under this year. A franchise in Houston recently filed for Chapter 11 bankruptcy protection, and dozens of other franchises are reportedly up for sale at a discount.

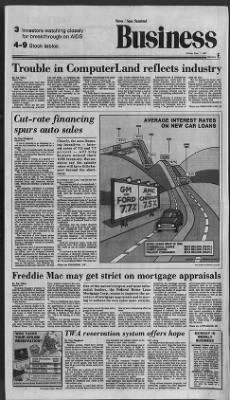

Some of the larger ComputerLand stores, many of which generate millions of dollars in sales monthly, may well break with the parent organization and strike in By Jim Talley Batista Writer ComputerLand Corp. may wish the song Only in Miami applied to its troubled franchise system. Last week the Hayward, company acknowledged the financial troubles of its Miami franchise, which about two weeks ago closed its five stores in Broward and Dade counties, while a buyer or another investor is sought. However, that's not the only franchise encountering problems. AVERAGE INTEREST RATES ON NEW CAR LOANS Cut-rote financing spurs auto sales 1982 1831 Clearly, the auto financing incentives interest rates of 7.5 and 7.7 percent will help dealers unload their 1985 inventory.

But analysts say the splashy rates will have little impact beyond the 1983 fl6.8! jrJi 1984 -Ti2 JUNE pi91. 1985 0 1 Vss. xXjiX i3.jj Nw. 12.6'y1. 7 rfc Villi -MA 0 7 By Tom Stieghorst Bwioen Writer If you're planning to go shopping for a new car this afternoon, be prepared for a crowd.

"The sales are unbelievable. It's almost like there's a waiting line," warns Daniel Meloche, a salesman for Maroone Chevrolet in Hollywood. The reason, ef course, is a special 7.7 percent finance rate offered on car loans by the nation's automakers. Since it was announced by General Motors two weeks ago, South Florida car dealers report a surge of new interest in car buying. The 7.7 rate is the lowest ever offered by General Motors Acceptance the financing arm of GM.

It was promptly matched by Ford Motor and bested by Chrysler Corp. and American Motors which are offering 7.5 percent financing. The programs, scheduled to continue through the start of October, are the most extensive incentives offered by Detroit in several years. And the 7.7 percent rate represents a discount of more than 40 percent from the average rate of about 13 percent now offered by commercial banks. Given those numbers, car sales have already improved and will probably soar in September.

Clearly, the incentives will help dealers unload their 1985 inventory. But analysts say the splashy rates will have little impact beyond the short-term. "These kinds of programs don't have any permanent effect on the market," says Maryann Keller, an automotive analyst for Vilas Fischer Associates, a New York investment company. "All it does is make people who were going to buy a car sometime in the fall buy one now," she says. The relaxation of auto import quotas combined with the current drift in the economy have most brokerage firms predicting a substantial decline in domestic auto sales in 1986.

But for now, the 7.7 percent financing is moving cars. John Andrew, a spokesman for GMAC, said the company received 300,000 applications for financing in the week after its program was announced, compared to 170,000 the week before. "I'd have to say it's increased our business by 100 percent," said Meloche, the salesman for Maroone Chevrolet. He says he's selling a car a day, "and I'm not that great a salesman." "Business has picked up tremendously," agreed Stetson Wallace, sales manager at Bill Wallace Ford in Delray Beach, who estimated sales rose 50 percent in the week after the financing moves were made. Not everyone is thrilled.

"I love it, but my finance department hates it," said one salesman at another Ford dealership. Stacks of loan applications will keep clerical workers busy at many dealers until the program ends. On the other hand, bank workers could have a light month. "Quite obviously, we've seen the volume fall off with auto paper," says Ray Sandhagen, executive vice president at Landmark Bank in Fort Lauderdale. Sandhagen says the bank's standard 12.25 percent rate on 48-month auto loans is very competitive with other banks, which nationwide make about half of all auto loans.

"But if somebody's looking at 7.7 percent financing the commercial banks can't compete with that rate," he says. Until the incentives expire, banks will primarily serve their existing customers who come in out of loyalty, Sandhagen said. It's not hard to see why. By financing at 7.7 percent, a Chevrolet Citation with a base sticker price of $7,090 would have a total financing cost over 48 months of $1,170, according to GMAC. The same pur- Please see FINANCING, HE AUTO LOANS HELD IN 1934: COMMERCIAL BANKS $35.5 BILLION (50.3) CREDIT UNIONS $32.4 BILLION (19.1) FINANCE COMPANIES $51.9 BILLION (30.6) Z7 SOURCE: fEDERAl RESERVE BOARO 1 Staff graphic by BONNIE LALLKY Freddie Mac may get strict on mortgage appraisals One of the nation's largest and most influential lenders, the Federal Home Loan Mortgage wants to improve the accuracy of mortgage appraisals and is moving to enforce its own rules more strictly.

zero-coupon bonds. Currently many appraisers often do not properly account for these incentives, Seale noted, with the result that home appraisals include the value of the creative financing as well as the value of the real estate. Stricter enforcement would require appraised values to be stated "in terms of cash or in terms ot wants to improve the accuracy of mortgage appraisals. And with the current economic environment vastly different from that of five or 10 years ago, Freddie Mac, as it is commonly called, is moving to enforce its own rules more strictly. "They're redefining their definition of market value, and it'll affect the appreciation of one's home," said Doug Parker, regional manager of Sunbank Mortgage Co.

in Orlando, a division of Sun Banks Inc. "We're all looking at it very closely." Builders are paying attention, too, since the change affects special sales incentives that make home-buying more affordable for first- incentives, the mortgage package will be adjusted, probably requiring a higher down payment and decreasing the number of people who can afford the purchase. Freddie Mac's vice president of mortgage operations, Leady Seale said in a recent letter to building and finance industry executives that his organization is considering requiring appraisers to use a "cash equivalency" approach, a method designed to discount the market values of homes to account for financing incentives that accompanied their sale. Such incentives include a wide variety of techniques, from builder buydowns and seller-assisted, low-rate financing to cash rebates and By Jim Talley Buineti Writer President Reagan's proposal to limit the deductibility of mortgage interest paid on second homes already has thrown a chill into real estate sales. But now another problem for the real estate industry is on the horizon.

The issue, centers on property appraising, an esoteric subject to be sure. But it could affect the market value of thousands of new and resale homes in South Florida and nationwide something more readily understood by homeowners, builders and others involved. One of the country's two largest and most influential lenders, the Federal Home Loan Mortgage financial arrangements equivalent to cash." The new approach would also require appraisers to deter- mine the "most probable price'? a home would bring in the market-' place, rather than "the highest price" it could bring traditionally the norm. Please see APPRAISALS, 2E have at least a dampening effect on sales." A buydown is a mortgage interest rate subsidy during the first few years of a loan, where the buyer makes a substantial down payment in exchange for a below-market interest rate. If appraisals are required to itemize the value of such time buyers, one of the most active groups in the market Chuck Lennon, executive director of the South Florida Builders Association in Miami, said that with the peak home sales period coming up this fall and next spring, "anything that eliminates or curtails the builder buydown would TWA reservation system offers hope WHO TAKES YOUR AIRLINE MONDAY IN WEEKLY BUSINESS By Tom Stieghorst RESERVATION? i Writer Mark! hare AlrlliM (Reservation system) i-i long benefited the industry giants at the expense of most other carriers.

Until recently, the most serious type of bias involved the display of flight information on a travel agent's computer screen. More than 90 percent of the 26,000 U.S. travel agencies now rely on computers to decide which flights to book for their clients. In the past, computer "vendors" iike United and American had programmed their systems to list their flights first when viewed on computer screens by the travel agent, ahead of competitors. But in 1984, the Civil Aeronautics Board prohibited such preferential set-ups on a vendor's primary computer system.

United, American and TWA signed another agreement this March with the Department of Transportation to end bias on secondary computer systems they were allegedly using txyskirt the intent of the CAB ruling. But despite these advances, other carriers continue to worry about the lack of an independent system. "They eliminated one form of bias, but they did not eliminate all forms of bias," says Bruce Cunningham, project director for the Neutral Industry Booking System Interest Group (NIBSIG), the 26-airline venture. For example, when travelers use more than one airline to make their trip, travel agents must decide which airline will initially collect the revenue for the flight and later distribute it to other airlines. Especially on international flights, where collection can take up to a year, the "float" earnings can be significant for the airline that originally "plates," or writes, the ticket.

Using various computer programs and commands, vendors can often designate Please see RESERVATIONS, 2E RETIRING YOUNG: Early retirement begins with early -planning, but it's not Impoa- tibia If you're willing to pinch pennies while young. Planning early retirement ia like piecing together a puzzle: By putting together the right pieces, financial planners tell Weekly Business, people In middle- to upper. Income brackets can build sizable nest eggs. PERSONAL FINANCE: What would you do If you Inherited Weekly Business advisers suggest the right Investments, and examine how to handle finan- ces after the death of a spouse. Smaller airlines, which have always feared the clout of American Airlines and United Airlines in the computer reservation game, are getting closer to ending their dependency on the Sabre and Apollo computer systems run by those carriers.

The two big airlines have long dominated the computer reservation systems used by travel agents, who book more than 60 percent of the airline seats flown each year. Two weeks ago, a group of 26 major U.S. and foreign airlines offered to buy TWA's competing reservation system, called PARS (Passenger Airline Reservation System), to combat the advantages enjoyed by American and United in the reservations area. If they succeed, it could limit the so-called bias in airline Reservations that has United (Apollo) 28 fcastem (Soda) 15 P1? 'T National market share based on number of travel agent locations -s SOURCE: Neutral Industry Booking System Interest Group Staff graphic byUY ELLEN.

Get access to Newspapers.com

- The largest online newspaper archive

- 300+ newspapers from the 1700's - 2000's

- Millions of additional pages added every month

Publisher Extra® Newspapers

- Exclusive licensed content from premium publishers like the Fort Lauderdale News

- Archives through last month

- Continually updated

About Fort Lauderdale News Archive

- Pages Available:

- 1,724,617

- Years Available:

- 1925-1991